Today is the final part of a four-part series on the Future of the MetroCard and smart card technologies. Part 1 outlined the benefits of smart card technology; Part 2 outlined the deficiencies of the MetroCard; Part 3 summarized the current plans for a smart card in NYC; and Part 4, below, proposes a new smart card for NYC.

The NY Times this morning had additional coverage on Bloomberg’s free cross-town bus proposal, as well as his push for a NYC smart card. According to the article, Mr. Soffin, an MTA spokesman, insisted that the MTA’s pay-pass pilot (on the Lexington Avenue Line) would be expanded to some buses by the end of the year. No word on a potential link with the Port Authority or New Jersey Transit, as the Philadelphia Daily News reported in July.

Part 4 – Get Smart

Although the specifics remain unclear, there are enough whispers from Elliot Sander, Jay Walder, Bloomberg, and the Port Authority to glean that an inter-agency smart card (in some form) is on its way. Outlined below is a proposal for what I believe such a smart card should look like in NYC.

A fantasy smart-card for NYC. Could this be our future?

1. Contactless RFID-Chips

I admit that I do not understand all of the technology behind fare cards, but I can say with certainty that the magnetic strip technology of the current MetroCard is not capable of performing all of the functions of a full-fledged smart card. Smart cards use an RFID chip, which enables a greater amount of information to be stored on a card than on a magnetic strip. Many credit card companies have supplemented magnetic strips with RFID chips on their own credit cards, because the capacity of RFID offers space for security features that permit users to use the card without a PIN. These same security features enable transit agencies to create smart card management systems for riders online. Additionally, the capacity of RFID allows one card to carry multiple pieces of transit information: an unlimited pass, a user’s transit status (student, handicapped, senior, etc.), transit balance, etc..

In addition to holding a greater capacity, RFID chips are also incredibly durable and adaptable. Even if a magnetic strip could implement all of the technological benefits of an RFID chip, it would have to be replaced at least as often as the average, well-used debit card. And unlike magnetic strips, an RFID chip can be embedded into virtually anything: cell phones, key chains, and even bizarre, carbon-tracking gloves. In Hong Kong and Britain, transit RFID chips are embedded into bank debit cards, streamlining wallets with one fewer card and enabling users to re-fill their transit accounts at bank ATMs.

Yet let’s take this a step further. Imagine a day when you can buy your transit tickets and passes on your smart phone. When you arrive at a fair gate or enter a train, instead of waving your smart card over a sensor – you’ll wave your RFID-embedded phone. In other words, your phone has become both the ticket vending machine AND the ticket. No MetroCard will ever be able to do that.

Finally and most importantly, RFID chips enable Contact-Less payment. While the MetroCard seems relatively fast, anyone who has used a contact-less smart card will tell you that it’s slow and prone to error. Currently the NYC subway system is bursting at the seams with over 5M riders on a weekday, and that number will continue to grow. A fast fare payment system will reduce congestion at subway turnstiles and dramatically speed payment on buses.

2. Inter-modal Compatibility

Like the Oyster and the Octopus, NYC’s smart card must be inter-modal. As outlined on Monday, the smart card has the power to remove psychological and logistical barriers between transit systems and modes. Once those barriers are removed, transit systems see greater flow between complementary, connecting modes.

As readers mentioned in their comments, implementation on each respective mode will require coordination and planning. While subways have logical entry and exit points, commuter rail lines do not. International systems, however, offer many examples of successful implementation on different modes of transportation. On the National Railway in London, conductors carry digital readers that scan the smart cards. Each rider’s card has a monthly pass, a digital one-way ticket purchased on the platform, or a fund to debit the ticket purchase. The flexibility of the technology ensures successful, inter-modal implementation.

3. MTA, Lead the Way! Sort of. . .

The politics of creating a regional smart card for NYC will undoubtedly be complicated. On the one hand, the Port Authority has traditionally played the role of inter-state transit leader. In order for the smart card to be a success, however, the MTA will play the most important role.

As outlined yesterday, the Port Authority has already implemented SmartLink, a smart card that has many of the features of modern smart card technology. Not only is it contact-less, like the Oyster or the Octopus, but its value can be controlled through the SmartLink website. The PA’s pilot for an expanded smart card system presumably will utilize the SmartLink.

A smart card in NYC, however, must be implemented first on the NYC Subway and NYC buses, because it the most efficient way to achieve a critical mass of smart card users. Unlike on commuter rail systems, smart card implementation on the subways/buses will be straightforward both for the MTA and most riders. Furthermore, since subway and bus ridership are so large relative to all other systems, smart card success on these modes would encourage its success on other modes/systems. Riders will gravitate to the fare card they use most frequently or is most popular.

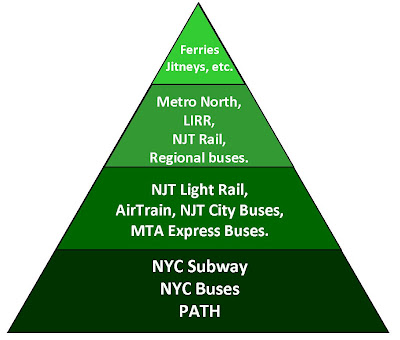

As a result, implementation of a NYC smart card should follow a pattern that first establishes mass acceptance and then builds upon that foundation to link other systems that do not traditionally share the same fare collection system:

A. Start with systems where implementation is straightforward, ridership is greatest, and services are already linked: NYC Subway & Buses.

B. Extend implementation to popular connecting services that are intuitive extensions of the existing implementation: PATH, Hudson-Bergen Light Rail, Newark Light Rail, NJT Local Buses, AirTrain, etc

C. Extend to connecting systems that require more complex implementation and potentially contradict users’ traditional payment methods: LIRR, Metro North, NJT, Regional Buses, etc.

D. Extend to systems with lower ridership: Ferries, private jitneys, etc.

Although this project must rely on the MTA’s participation in order to achieve success, it should not be, nor can be, the sole agency leading its design. In my opinion, the Port Authority is unique in NYC for its role in bridging different governments and transit systems. Furthermore, the SmartLink card has already been successfully developed and piloted on the PATH. As a result, the MTA should not build their own smart card. Instead, they should take advantage of the Port Authority’s already completed R&D work by adopting the SmartLink and then working with the Port Authority to spread it to other systems.

4. Super-Regional Compatibility

Several readers expressed concerns about the boundaries of a NYC smart card. Reader Avi remarks:

“But once you add NJ Transit you open up a whole new can of worms. NJ Transit shares a station (Trenton) with Septa. Do you add Septa to the system? What about the NJ Riverlines? PATCO? It’s easy to keep saying yes, yes, yes, but before you know it you’re trying to coordinate an agreement between 10+ different agencies in 5+ states. Good luck getting everyone to agree on that.”

First, thank you, Avi, for your comment – it’s a very important point. Before I address it, I would like to remind everyone that we shouldn’t limit our plans simply because they seem complicated or overly ambitious. If planners had felt the same way 100 years ago, we never would have built NY’s current subway system.

Second, don’t underestimate the power of the smart card. If the Philadelphia area issued its own smart card for SEPTA, PATCO, and NJT services in the Philly area, there is no reason why this system could not be compatible with New York’s system. On Massachusetts highways, for example, the toll collection system is Fast Lane, but is fully compatible with EZ-Pass. The technology of RFID chips and their linkage to credit cards and bank accounts could easily allow for cross-system compatibility. In fact, planners in Philly are already planning to ensure potential cross-compatibility, by creating an “open-loop system” that will allow any RFID-enabled device to pay for the services.

Even if we presume that cities – DC, Philly, New York, Boston – remain the epicenters of respective smart card systems, we can presume that each card can be designed or adapted to ensure cross-compatibility. As a result, services that exist on the border of two transit eco-systems, like the RiverLine (NY and Philly), can accept more than one smart card. Regardless of which card you use, the appropriate agency will still receive the fare.

24 comments

[…] MetroCard. Part 3, available here, summarizes the current plans for a smart card in NYC; and Part 4 proposes a new smart card for […]

Absolutely marvelous idea, but please don’t call it the “Liberty Card”. How about the “MetroSmart Card”?

Personally, I’d rather have a card separate from my phone. But if people want to have that option then that’s fine.

Keep in mind that unless the card system is standardized nationally (perhaps this something a credit card company would be intereted in working on) you are still going to need to vend cheap, disposable tickets for those who are just visiting or use the system too infrequently to warrant getting a permanent card. I’m not sure RFID is cost effective for disposable tickets. Correct me if I’m wrong.

In LA the physical smart card costs $2 (when they rolled it out they gave out a ton for free, but if you buy one now it’s $2). They’re not required for single rides, though – you can still pay cash for a single ride and (I believe) get a disposable paper ticket. You only NEED the smart card if you want to get a pass or anything like that. And since LA has no free transfers between lines, you’ll want that day pass most of the time.

However, they’re apparently putting turnstiles in all the subway entrances now (before it was the honor system with random fare checks), so I’m not sure how that affects paying for single rides.

I used a CharlieCard for a bit in Boston and it’s nice, but I definitely would refrain from letting it be tied to a credit card account as some have suggested with a smart card for the MTA. RFID is hackable. It’s been demonstrated how easy it is to steal info from an RFID chip. Then it’s just a matter of cracking any encryption. Which MIT kids showed how to do for the CharlieCard.

I think a key to the sucess of the octopus card in hong kong is that octopus was designed to be an independent company, which it is now. It is an independent company that work to get as many people to use it everywhere.

It is also important that this smartcards are independent from anything else. Ie, not directly linked to a credit card or identity. No one wants to be tracked nor deal with credit history issues is they lose their card.

If EZ Pass is multi-regional, then it’s transit card equal should be too. Open loop systems also allow cards from different manufactures to work on the same platform.

How great would it be if someone from New York could take there fare card & travel to Chicago, Los angeles, Seattle or any other city that allowed the use of there current card. Better yet, what about tourests who ride transit back home who pay with a smart card could use it to pay fares while visiting the big apple. That way all a tourest would need to do is add funds at a vending machine wich lowers transaction time per person.

You should see the ongoing train wreck with smart cards in the San Francisco Bay Area, where we have even more cooks in the kitchen. One agency, the Bay Area Rapid Transit District (BART), went ahead and promoted its own EZRider smart card, even as the regional coordinating agency, the Metropolitan Transportation Commission (MTC), was developing a multi-agency TransLink card. Integration of fare systems and rollout of the TransLink card has been slow, with some agencies reportedly dragged kicking and screaming into the agreement.

All of the components of Oyster are open source, allowing it to be compatible with future smart cards for other UK transport systems. Also, Oyster has top-up fees and automatic refills, something I think could be quite handy and the MTA has already started to work on. How many times have you been in a rush and had just a bit under $2.25 (or $2)? If we did what’s done in London, your card would bounce back up to a certain amount when it hits $3 or something along that line, making it easier to catch the train right before it leaves the station.

LibertyCard would actually be a nice pun (liberty/freedom to travel around the entire metropolitan area), but I think SmartLink is better.

I like “Liberty Card”. Liberty is exactly what it gives you. Or if it has to be named after a food, how about “[Big] Apple Card”? Or does it have to be seafood? “Squid Card”…?

Boston and Washington, DC both have contactless smartcards. It would be great if the NYC/Boston/DC/Philly/etc. systems all were at least compatible with each other at the level of deducting cash on a pay-per-ride basis (probably not for the purposes of buying a montly unlimited pass or what have you).

Of course that raises some other technological issues. Boston has a similar flat fare for any ride model, but DC has variable fare so it needs to track both your entry and exit station before deducting cash.

Given the amount of business travel between these cities, a compatible smartcard system would be great. Now if only Amtrak were cheaper.

OMG…I’ve been using the term “Liberty Card” as the name of a future smartcard for NYC for years! Copycat! 🙂 (Originally chose “Freedom Card” but Chase released some credit card with the same name.

If RFID is the route, its all ready here. RFID payment systems are all ready ubiquitous in the New York metropolitan area. Our largest banks (Chase, Citi, BofA, Barclays – all of them?) have cards with the chips in them.. Look at your Chase card. If it says BLINK on it – you’re all ready RFID capable. Seems that 50 million RFID cards were issued last year alone in the US. It’s here. No reason to duplicate it (other than the ‘branding benefits’ of having a transit card (I’ll admit its a nice thought).

Simply, the MTA, PATH, NJT, NY Waterway, etc. should accept the standard bank RFID issued payment cards. Consumers can use their own PC’s, terminals, converse with a commuter train conductor or visit agents in major stations to ‘arrange a trip’ or ‘set up’ their account for special programs: monthly unlimited, easy pay.

New programs developed by the fare consortium perhaps – LIBERTY PASS – unlimited usage all systems (a particular operator can share in the fee based on the pro-rata usage reported each month)

I presume the issue is that agencies don’t want to pay 2% of the fare box to banks. Although one must consider if the SAVINGS from not ceasing to operate their own individual fare ecosystems will be far greater than any commission paid.

In any event, the consortium should require the banks advance the costs of conversion of all systems and fund centralized start up operations (a very consumer friendly web portal). My bet is the consortium will have such volume to offer they can dictate the commission they’re willing to pay (my guess less than 1.25%). The residual benefits to the banks will be tremendous financially. The RFID universe will light up.

What do you think?

Another great thing about having an RFID chip be the basis of new SmartCard technology is that you can change and upgrade the cards without having to redo the whole fare collection system. For example, right now no one has cell phones that can do what you described, so it would be pointless to develop a system that worked for cell phones and nothing else. But if you start out with cards with an RFID chip, then later you can expand that by putting the same type of RFID chip in anything — cell phones, gloves, whatever.

It’s easy to keep saying yes, yes, yes, but before you know it you’re trying to coordinate an agreement between 10+ different agencies in 5+ states. Good luck getting everyone to agree on that.”

I’ve had an RFID tag velcro’d to my car’s windshield for years. It’s good in 13 states and once Ohio gets up and running you can pay tolls from Maine to Illinois with it.

A trip from suburban Philadelphia to Long Island means that the PA Turnpike, the Delaware bridge authority, the New Jersey Turnpike, the Port Authority and the MTA all had to agree on a standard. Same trip on mass transit would involve three transit agencies, SEPTA, NJ Transit and the MTA… they could work it out…

So here’s my question in all this. Why hasn’t the example of the Netherlands been brought up in all this? From a look at their “OV-chipkaart” it is exactly the type of regional solution we could use. They offer 3 different types of cards that are available which cater to different types of users of the system. Once these cards start handling more “value” they will need to be linked to individuals which would allow for proof of theft or loss. But at the same time, anonymous cards are available so as to quell the nerves of those thinking “big brother” is on the rise. Granted those anonymous cards have less features associated with them, but they are available non the less. Additionally, they offer cards which are promoted directly towards tourists which offer unlimited transit for a flat rate over the course of a stay. See the GVB website here for an example of the types they provide: http://www.gvb.nl/english/trav.....hcard.aspx

This is by far what I would consider the “holy grail” of transit systems and smart card management.

Anyone who’s tried to work their way onto the 7 train after a Mets game would agree that Metrocards can be awfully slow.

A word of warning from London – phasing the introduction across different modes of transit can have dire consequences. For example – In London, you can use Oyster on both Commuter Rail services and on the Underground (subway). However, when using commuter rail, you can only use the ‘unlimited ride’ function. You can’t use the pay-and-go system.

This can lead to the absurd situation of using pay-as-you-go for the tube, and then having to stop to buy a paper ticket when transferring to rail, EVEN THOUGH the rail stations are fully equipped with Oyster Readers.

(Also a minor correction to part one of the series – the Oyster Card system is in fact administered privately, not publicly. I discovered this when my wallet was stolen, including the Oyster Card with an expensive 6-month unlimited ride card pre-loaded onto it. I assumed they would easily be able to cancel the old card and re-issue another with the same value loaded on. In fact, London Underground weren’t able to help and I had to go to Oyster directly.)

I can’t wait to get “SMART”.

I’m surprised there has been no discussion of the privacy concerns of RFID cards here. RFID can be read at a distance with a radio transmitter and receiver. With a directional antenna, that could be a significant distance. Since the RFID card has unique identifiers on it (such as a card number or a customer number), the card can be used to track people at a distance, while people are not even using the transit system.

See for example:

Video: Hacker war drives San Francisco cloning RFID passports

Feds at DefCon Alarmed After RFIDs Scanned

-Chris

In fact, the card should be fully interoperable with SEPTA in the future. SEPTA is currently developing a Smart Card for their system, and it is being designed to be open-ended, specifically so it can be integrated with potential future transit payment systems that link to SEPTA (inferring NJ Transit without specifically naming them).

Excellent post! This is the type of info that should be around the internet. Shame on Bing for not positioning this post higher

Woah this blog is wonderful i really like studying your articles. Stay up the good paintings! You know, lots of persons are searching round for this information, you can help them greatly.

Valuable information. Fortunate me I found your website by chance, and I’m surprised why this accident didn’t came about earlier! I bookmarked it.

I simply couldn’t leave your website before suggesting that I

actually enjoyed the usual info an individual provide to your visitors?

Is gonna be again continuously to check up on new posts